- Investor Security

- September 24, 2025

Table of Contents

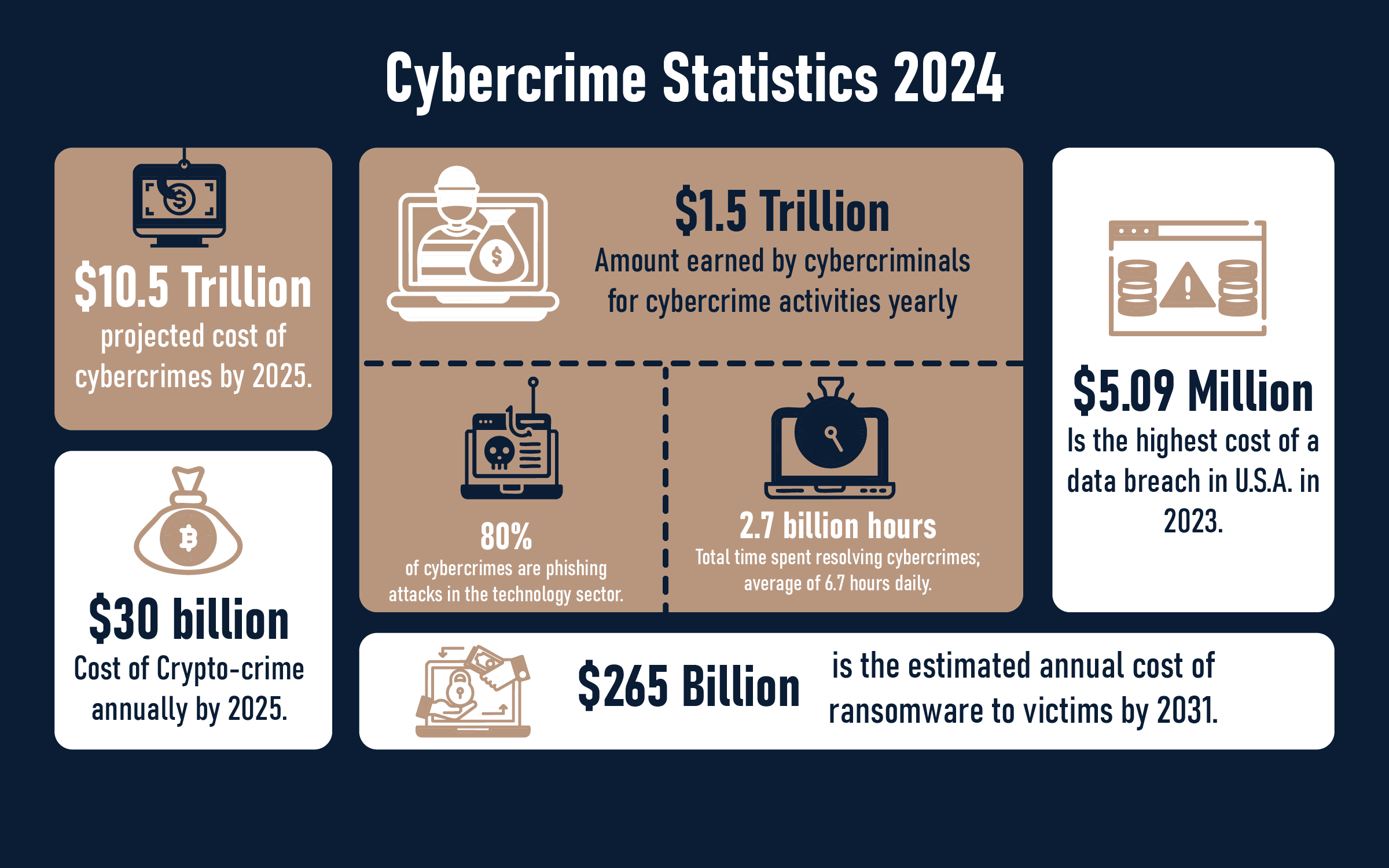

Financial fraud in the United States alone costs Americans a staggering 12.5 billion dollars in 2024. Concurrently, global damage from cybercrime hit in excess of 16 billion dollars and is a bitter reminder of how vulnerable our virtual monetary world is in the course of becoming. Through online banks and cell phone investing, and a multitude of other online money programs, consumers operate an ever-growing number of money transactions online compared to the past. With convenience comes increased vulnerability.

Following an increase of 33 percent in 2023-2024, as estimated by the FBI, internet crime losses were primarily linked to payment redirection ploys, phishing schemes, and investment scams. Constantly rising online payments are turning cyberthieves into savvy, effective, and elusive operators. Your balance in a banking app, a digital wallet-based wire transaction, or crypto is in their sights, no matter how one chooses to look at it.

How do we protect ourselves?

This ultimate guide will cover absolutely everything you ever wanted to know about online banking security, online payment safety, and how to invest safely. With support from the latest figures and best practice, you will discover how to:

- Create safe banking and investment accounts

- Avoid and recognize phishing scams and fraud traps

- Use mobile apps and payment platforms safely

- Develop a family emergency plan

At the end of it all, you'll have practical steps to keep your money, accounts, and identity safe online—so you can bank, pay, and invest safely.

Understanding Online Financial Security

Money management online is a habitual behavior, but is now performed within a dynamic risk-intensive environment. Protection of finances depends on an understanding of how online financial crime is committed, how it is affected by trends, and why digital bank fears are outdated.

The Current State of Online Financial Crime

Online financial threats have reached historic highs. The numbers below illustrate the alarming scale of cybercrime targeting everyday users and investors:

|

Type Of Fraud |

2024 Loses |

Growth Rate |

|

Investment Scams |

$5.7 billion |

+24% |

|

Internet Crime Total |

$16+ billion |

+33% |

|

Cryptocurrency Fraud |

$5.6 billion |

+45% |

|

Business Email Compromise |

$2.7 billion |

[FBI data] |

|

Tech Support Scams |

$1.4 billion |

[FBI data] |

These figures reflect not just higher monetary losses—but also increasingly sophisticated tactics used by fraudsters to exploit trust, urgency, and digital access points.

Key 2024–2025 Trends

Fraudsters who are dealing with cyber stuff are targeting individuals as well as companies using their constantly changing scams. The main trends that ought to be known are:

- Investment frauds keep being the main category both by the number of cases and by the money lost

- In 2024, 83% of the surveyed companies report that insider threats had caused them issues

- The average data breach-related costs have increased to $4.88 million, which is a 10% rise on a global scale

- The cost of cybercrime is projected to reach $10.5 trillion annually by the year 2025

- The number of payment redirection fraud incidents (e.g., invoice fraud) has increased by 66.6% in 2024

Such is the situation with trends that stress the need for intemperate security while money matters and vigilance while investments to escape the trickery of the fraudsters.

Why Online Banking Is Actually Safer Than Traditional Methods?

Online banking done properly can be much safer than the traditional ways everybody has in mind, such as paper-based or face-to-face transactions.

- Data being transferred or updated is not accessible by third parties, as it is encrypted

- Frequent notifications and constant surveillance instantly catch the impostors who try to do fraudulent activities

- A user has to pass identity verification more than once when it comes to multi-factor authentication; thus, a hacker has minimal chances to break in

- Moreover, there is an assurance program which is called FDIC, which is said to be for absolutely safe deposits of a bank owner, no matter if the account is online or offline

Common Myths About Online Financial Security

Let’s bust some outdated beliefs:

Myth: Paper-based account summaries give more security than digital ones

Truth: Even though paper might be stolen or lost, checking and control over accounts in real-time and the usage of encryption to prevent unauthorized access put digital records far ahead in terms of safety

Myth: Applications for banking on the go present more security risks than websites

Truth: Mobile platforms often come with biometrics to help users' identity, plus less susceptibility to phishing attacks than browsers

The first thing you need to do in order to guard your money and life on the internet is to come to grips with the online world and the false beliefs that are present.

Essential Online Banking Safety Practices

Even with every other cybersecurity infrastructure intact, online banking safety starts with one's own habits. These best practices mitigate the potential for fraud, identity theft, and unauthorized access.

Password Security and Authentication

A password acts as the very first line of defense. Weak credentials or credentials shared across accounts are just two of the many common entryways into a system used by attackers.

Strong Password Requirements

- At least 12-16 characters

- Use a combination of uppercase and lowercase letters, numbers, and symbols

- Never use the same password for different accounts

- Use a password manager for storing and generating passwords. Some examples include Bitwarden, 1Password, and Dashlane

Two-Factor Authentication (2FA)

- Offers a second confirmation of identity (via, for example, text codes or biometric tests)

- Prevents someone from gaining entry when they have successfully guessed or stolen your password

- Typically, when you log in with your credentials to the bank website, there will be an option to enable 2FA from the settings screen. This option is normally well hidden in security settings in your account dashboard.

Tip: Go with an app-based authenticator like Google Authenticator or Authy instead of SMS codes, as the latter can get intercepted.

Secure Connection Practices

Protect your online banking sessions with a strong network and device hygiene.

Network Security

- Never use public Wi-Fi for banking or payments

- Always look for HTTPS and a padlock symbol in your browser

- Use a VPN (Virtual Private Network) for extra encryption

- Secure your home Wi-Fi: change default router passwords and enable WPA3 or WPA2 encryption

Device Security

- Keep your OS, browser, and apps updated regularly

- Install reputable antivirus and anti-malware software

- Lock your phone and use biometric login features

- Always log out of banking sessions—don’t just close the tab

Digital payment security starts with your device. If it's compromised, so is your account.

Account Monitoring and Alerts

Early detection is key to minimizing losses.

Daily Monitoring Best Practices

- Check all your accounts at least once a day or every few days

- Review transaction history carefully—don’t ignore small charges

- Report any suspicious activity within 60 days to remain eligible for reimbursement

- Immediately freeze cards or accounts if anything looks off

Alert Setup Guide

- Balance alerts: get notified if funds drop below a threshold

- Transaction alerts: for all purchases or those over a set amount

- Large purchase alerts: flag anything unusual

- Login attempt notifications: get notified of suspicious sign-in attempts

Enable alerts through your bank’s mobile app or online settings—it takes just a minute.

Recognizing and Avoiding Phishing Attacks

Phishing scams trick users into revealing credentials or installing malware. Be extra cautious.

Common Phishing Tactics

- Emails pretending to be from your bank asking for “urgent” action

- Links that lead to fake (but convincing) login pages

- Attachments claiming to be invoices, receipts, or statements

- Pop-up ads or calls pretending to be tech support

Verification Methods

- Don’t click on links from unsolicited emails—type the bank’s URL directly

- Check email headers and domain names for fakes

- Contact your bank via official channels if something seems suspicious

- Banks will never ask for your password, OTP, or full card number via email or text

If you're ever unsure, pause and verify—it's your strongest defense against financial phishing scams.

Secure Online Payment Methods

Whether you’re buying groceries online, paying bills, or sending money to a friend, digital payment security is essential. Understanding the safety features and risks of different payment methods helps you avoid fraud and keep your financial information secure.

Traditional Online Payments

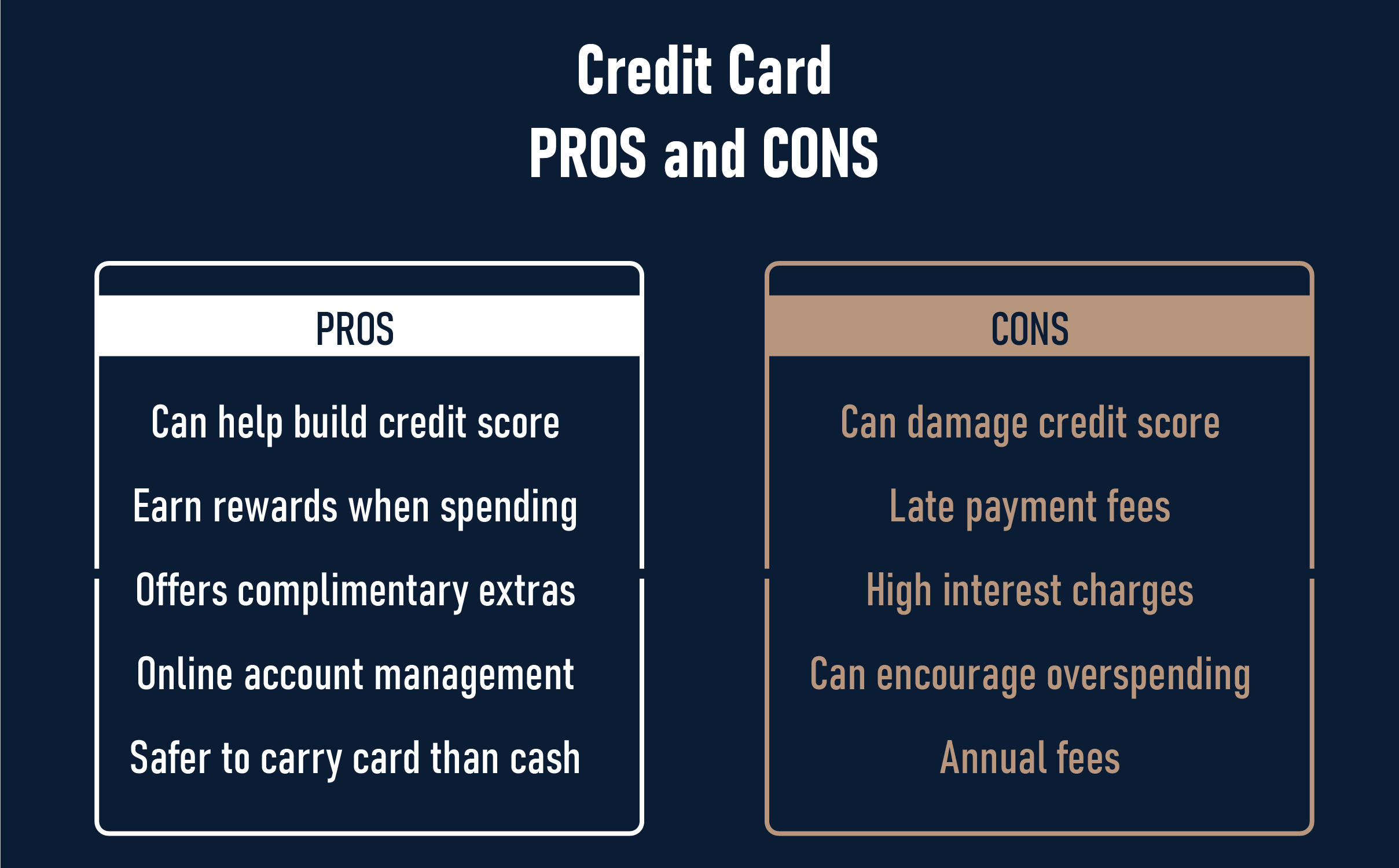

Credit Card vs. Debit Card Security

When it comes to secure online payments, credit cards offer better protection than debit cards:

Credit Cards

- Limited liability for unauthorized charges (typically $0)

- Transactions don’t directly impact your bank balance

- Easier to dispute fraudulent activity

Debit Cards

- Directly connected to your checking account—money leaves instantly

- Limited protection if fraud isn’t reported promptly

- It may take longer to recover lost funds

Best practice: Use credit cards for all online purchases to reduce direct financial exposure.

Bill Pay Services

Many banks offer online bill pay as a secure way to automate recurring payments:

- Bank Bill Pay is typically safer and easier to manage than merchant autopay

- Avoids giving third parties direct access to your debit or credit card info

- Set payment reminders and monitor for unexpected charges

Review recurring payments monthly to ensure you’re not being overcharged or subscribed to unused services.

Modern Payment Platforms

Peer-to-Peer (P2P) Payments

Apps like Zelle, Venmo, and Cash App offer convenience, but not always buyer protection.

P2P Safety Tips

- Only send money to people you know and trust

- Double-check usernames and phone numbers before sending

- Avoid using P2P for purchases or services from strangers

Unlike credit cards, P2P transactions are often irreversible if sent to the wrong person.

Digital Wallets

Apple Pay, Google Pay, and PayPal add extra security layers via tokenization—your card number is never shared directly with merchants.

Best Practices

- Enable device-level protection (biometric or PIN)

- Avoid storing passwords or card numbers in unsecured notes/apps

- Use trusted platforms only

Check wallet activity regularly and disable cards if your device is lost or stolen.

E-commerce Security

Before you make a purchase online, always do a quick security check:

- Look for “https://” and the padlock icon in the address bar

- Avoid entering payment details on websites that look outdated, unprofessional, or full of ads

- Stick to reputable, verified merchants and marketplaces

If a deal seems too good to be true, it probably is. Stick to trusted sellers with clear return policies.

Investment Security and Fraud Prevention

Although it is more convenient to increase your assets with the help of digital platforms, the latter contributes to a higher number of investment frauds. Securing your investments, be it in stocks, crypto, or even retirement, can only be done through vigilance and an active security posture.

Common Investment Scams to Avoid

Investment scams are now the leading category of financial fraud by dollar losses. Below are the most prevalent scams and how to avoid them.

|

Scam Type |

Warning Signs |

2024 Impact |

Protection Method |

|

"Guaranteed Returns" |

Promises of no risk or fixed gains |

$5.7B total losses |

Research thoroughly and verify licenses |

|

Cryptocurrency Scams |

Urgency to invest, high-pressure sales |

$5.6B losses (+45%) |

Use regulated exchanges and secure wallets |

|

Romance Investment Scams |

Partner pushes crypto/stock schemes |

Median loss: $1,996 |

Verify identities and never mix romance with finance |

|

Tech Support Scams |

Pop-ups claiming threats, urgent calls |

$1.4B losses |

Never allow remote access to your device |

If it sounds too good to be true, it usually is. Always check for SEC registration, FINRA IDs, or platform legitimacy.

Protecting Your Investment Accounts

Your online investment accounts need at least as much protection as your bank accounts, if not more.

Account Security Tips

- Use FINRA-licensed brokers or platforms

- Set up real-time alerts for login attempts and transactions

- Log in regularly to check account activity

- Use strong and unique passwords, and enable two-factor authentication.

Due Diligence Process

Scammers take advantage of ignorance. Doing your homework can save you thousands.

Before investing, always:

- Use FINRA’s BrokerCheck or the SEC’s IAPD database to verify an advisor’s credentials.

- Research the company or investment – look for potential red flags in reviews and disclosures.

- Know the fee structures, potential losses, and lock-in periods.

- Have all terms and conditions of the investment in writing. This is particularly important for private placement offerings and those investments that offer a high return.

Don't be afraid to say no. A legitimate advisor will never rush you and will answer all your questions.

Cryptocurrency Security

Investors should be vigilant about the following features peculiar to crypto investments:

Key Crypto Safety Measures

- Use hardware wallets (Ledger, Trezor) for long-term storage.

- Make sure to store your private keys and recovery phrase offline and securely.

- Select reliable exchanges with sophisticated security measures and insurance.

- Enable all available account security features like two-factor authentication, a whitelist of withdrawal addresses, and cold storage in a wallet.

Lose your private key and you lose your crypto. Always keep backups of your keys (offline and encrypted).

Mobile Banking and App Security

More than 65% of banking customers now look to their smartphone to deal with their finances. From apps to phone-based wallets, your handset carries the key to your sensitive financial information and it requires protecting.

Choosing Secure Banking Apps

Make sure the apps are the authentic and secure ones linked to your bank and credit cards.

Best practices when choosing apps:

- Download apps only from Google Play or Apple App Store.

- Check permissions—does the app really need to access your location or contacts?

- Read user reviews and security ratings to look for reported fraud or data leaks.

- Upgrading apps to plug security holes.

Avoid downloading third-party APKs or copies because they often contain malware or spyware.

Mobile-Specific Security Measures

The phones are vulnerable to the following attacks.

Strengthen your mobile defenses:

- Create a strong screen lock (e.g., PIN, pattern, or password).

- Allow the application to be launched by biometrics (fingerprints, face recognition).

- Do not charge at public charging points (USBs have malware—always charge from your charger).

- If your app offers this option, use a separate PIN for the banking app.

- Use automatic locking after a short period of inactivity.

Lost or Stolen Device Protocol

Losing your device can quickly become a security nightmare—unless you're prepared.

Steps to take immediately:

- Use “Find My iPhone” or “Find My Device” to remotely lock or erase your phone

- Notify your bank and freeze or lock your mobile banking app

- Change all your passwords—especially for email, financial, and app accounts

- Report the loss to your mobile carrier and local authorities

- Consider enrolling in identity theft protection if financial apps were compromised

Preparation is everything. Enable remote wipe and backup options before a loss happens.

Creating a Personal Financial Security Plan

Staying safe online isn't about one-time fixes—it’s about building and maintaining strong habits. A personal financial security plan keeps you proactive, organized, and better prepared for emerging threats.

Security Checklist

Use this recurring checklist to stay ahead of financial fraud and protect your online accounts year-round.

Monthly Tasks

- Review all account statements for unauthorized activity

- Check your credit report via Equifax, Experian, or TransUnion

- Update passwords for banking, investment, and payment apps

- Verify alert settings for transactions, logins, and balance changes

Quarterly Tasks

- Review investment account performance and security settings

- Update security questions to keep answers unpredictable

- Check device security (antivirus, OS updates, biometric locks)

- Review emergency contacts for financial accounts or recovery options

- Consistency is key—set calendar reminders to complete these tasks.

Building Your Security Toolkit

Equipping yourself with the right digital tools can significantly improve your online banking safety and identity theft prevention strategy.

Recommended Tools

- Password Managers: Bitwarden, LastPass, 1Password (for secure and unique logins)

- Antivirus & Security Software: Norton 360, McAfee, or Bitdefender for real-time device protection

- Credit Monitoring Services: Experian, Credit Karma, or IdentityForce to detect fraud fast

- Identity Theft Protection: Services like LifeLock or Aura to handle account takeovers and recovery

Think of your security toolkit as a digital first-aid kit—essential for preventing and managing cyber threats.

Stay Safe, Grow Smartly

Your amount of money health is not defined by the intelligent money choices you make, but rather by the level of protection that you provide for your data. From online payment security and password hygiene to investment fraud loss prevention and mobile banking security, the more steps you take, the more effective your protection against the threats becomes.

What is good news? It is a fact that people can also stay safe on the Internet by using adequate knowledge and tools. With the help of the best practices listed in this guide, you will significantly decrease your chance of becoming a victim by monitoring the accounts, enabling alerts, using 2FA, avoiding phishing scams, and selecting secure apps.

Never has the time been so right to act. Check up on your financial security plan, change passwords, set alerts for fraud, and teach the people around you.

When it comes to online banking, online payment, and investment prospects, it is possible to be no less and even better secured than with the traditional variants of this same thing, provided that, of course, you are not sloppy. Digital money is worth safeguarding. Keep your eyes open wide, keep up to pace, and stay safe.

FAQs (Frequently Asked Questions)

Be wary of promises like “guaranteed returns” or “limited-time crypto opportunities.” Always:

- Verify the credentials of advisors via FINRA’s BrokerCheck or the SEC’s IAPD tool

- Research the company and read reviews from independent sources

- Avoid platforms that pressure you to invest quickly or offer unregulated services

- Never send money or share credentials based solely on social media or online messaging

Yes—banking apps are generally safer than web browsers when:

- Downloaded from official app stores

- Protected by biometric login (fingerprint or face ID)

- Set up with two-factor authentication

- Regularly updated to the latest version

- Avoid using unsecured Wi-Fi and always log out when done.

Phishing scams try to trick you into revealing personal information. Watch out for:

- Emails or texts with urgent language asking for account info

- Fake URLs that mimic your bank (e.g., “chase-secure.com”)

- Unexpected attachments or links

- Messages asking for verification via email or phone

- When in doubt, go directly to your bank’s official website.

A secure financial password should:

- Be 12–16+ characters long

- Include upper and lowercase letters, numbers, and symbols

- Be unique for each account

- Be stored in a password manager, not in notes or your browser

Follow these steps:

- Report it to your bank or financial provider immediately

- File a complaint with the Federal Trade Commission at reportfraud.ftc.gov

- Notify your local police department and request a report

- Contact credit bureaus to place a fraud alert or credit freeze

- Report investment scams via the SEC’s Complaint Center